What Are “Fair” Valuations For Private Markets?

Investments in private companies have slowed down. According to Fortune’s Term Sheet & KPMG, venture financing in the U.S. is down 24% from the first quarter and 34% below the record in the final quarter of 2021.

In addition to primary venture capital, over the last few months, I’ve been tracking secondary sales. As Pitchbook describes, “secondary deals — in which investors buy second-hand equity stakes from early backers, founders and employees”

Using this secondary data, I’ve been able to create a rough model for a Bid/Ask spread for VC.

I’ve noticed clear trends that are helping to paint a picture of the current state of the private markets and I’ve used the data to answer a few questions:

- What are the general trends in valuations?

- Why are fewer private companies being funded?

- What should a fair valuation be?

What are the general trends in valuations?

I’ve partnered with a number of founders directly, VCs, and secondary-specialized groups to gather price-per-share data. I’m tracking companies like Stripe, Figma, Ironclad, Opensea and others. (For the purpose of this post, I anonymize all specific company names)

Analyzing as a group, in a stacked area chart below, there’s a clear downward trend in prices. The chart represents the sum of all premiums and discounts, which means we can observe for this aggregate, how prices seem to be behaving and which are the companies that have the biggest movements as well as spreads from last round’s valuation.

There are definitely a few outliers here…

When removing them, there’s an even stronger downward trend, especially compared to May, when many companies were being priced with a premium and are currently showing discounts.

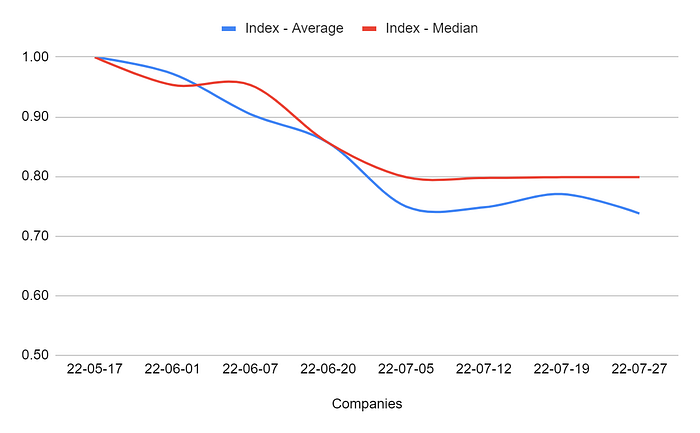

There are few companies that drove the average discount or premium up. However, the biggest takeaway from this data can be seen when looking at median change in price: the median secondary seller is now asking for close to a 15% discount in price from the last round.

Using this data on the average and median premiums/discounts to create an index, we can observe that from May to early July, there was a very strong downturn in the secondary market, which is now becoming more stable since then at this lower level.

Why are fewer private companies being funded?

There’s a disequilibrium between founders’ expectations & investors’ required return profiles.

Tom Tunguz, an MD from Redpoint, wrote a fantastic post about the VC spread. He said, “In the past few years, the spread has been tight. The market is liquid. Many startups sell shares to buyers at mutually attractive prices. Like the old stock trading floors with brokers yelling at each other, but in our era, we negotiate over Zoom coffees instead.”

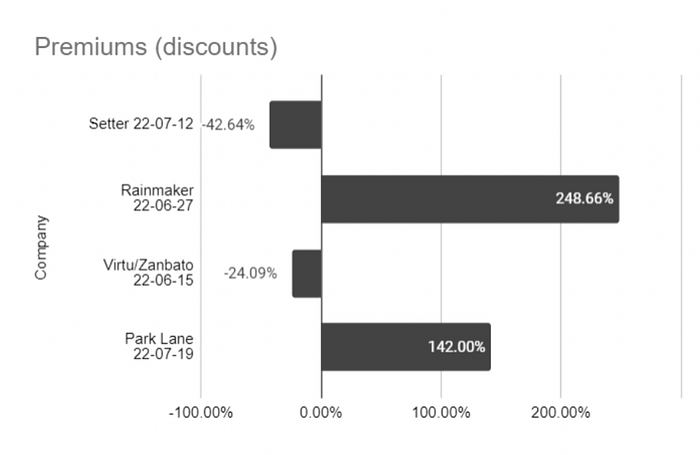

While the overall trend is down, upon looking closely at specific companies, almost all individually has a vast spread.

In Company 1 below, some sellers are asking for a 42.64% discount to the Company’s last funding round, while others are asking for a 248.66% premium.

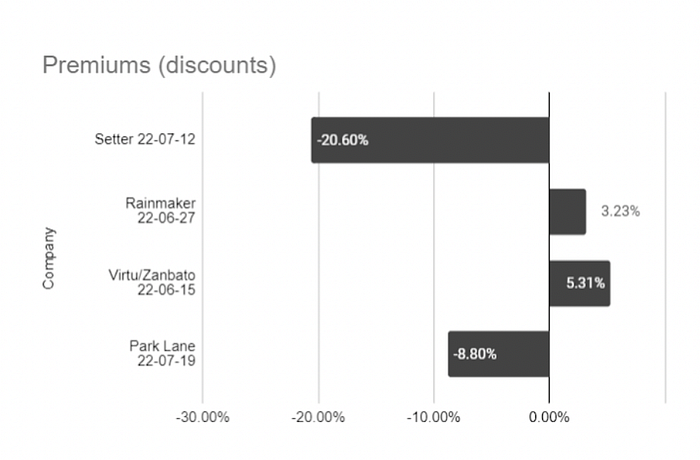

Here are other examples of premium/discount rates:

So why are fewer companies being funded right now? We don’t have an equal supply and demand.

If we take a step back and take a look at the performance of SaaS and Cloud companies in the public market, in Feb 2021 around the peak in valuations, these companies were trading on median at a 0.66x Growth Adjusted EV / NTM Revenue, and now this number is close to 0.19x, corresponding to a -71% adjustment in multiples, data according to Meritech.

Stock market comparables should imply private companies trade at a 50% or greater discount to the last round. But for a founder who previously raised a round at 100x ARR, they’re likely not willing to sell at such a steep discount.

What should fair valuations be?

It depends who you ask.

Let’s go back to Company 1. Its Price/Sales ratio, currently, is close to 21 times. Considering that the comparable multiples are at 4.2–2.8 times sales, here we have a simulation of the MOIC of a possible investment at different price discounts and revenue growth in a 3 year period (where I’d expect this company to IPO)

For Company 1, if I wanted to return 3.35x, a fair valuation from my perspective is a 70% discount — and Company 1 would still have to grow 70% YoY.

So while founders may be willing to sell at 15% discount rate, that might not be fair to VCs and their LPs.

Only time will tell how long it takes for the supply & demand prices to converge.

__

Thank you to my analyst Gustavo Trevelin for helping me track this data and model out the scenarios.